Governments and public sector institutions across Africa will face new expectations to disclose how climate risks affect public finances after the International Public Sector Accounting Standards Board (IPSASB) released its first global climate-related reporting standard for the public sector.

The standard, known as IPSASB SRS 1 on Climate-related Disclosures, is designed to help governments and public entities report how climate change creates financial risks and opportunities across their own operations, borrowing, and long-term fiscal sustainability. It is expected to influence how African governments access capital markets, manage climate risks and engage with development financiers.

The standard was approved in December 2025 and issued in January 2026, following a multi-year process initiated after the World Bank called on IPSASB in 2022 to develop public sector–specific sustainability reporting guidance. Until now, climate disclosure frameworks have largely focused on private companies, leaving a gap in how governments report climate-related financial exposure. It is expected to be effective on January 2028.

Governments across the Africa are among the most exposed globally to climate-related fiscal shocks, including droughts, floods and extreme weather events that strain public budgets, disrupt service delivery and increase borrowing needs.

Sovereign bonds account for roughly 40% of the global bond market, and many African governments rely heavily on debt issuance to finance infrastructure, energy systems and climate adaptation. Analysts say clearer disclosure of climate risks could affect how investors price African sovereign debt, particularly as climate impacts intensify.

Under the new standard, public sector entities, including national governments, regional authorities and state agencies, will be required to disclose material climate-related risks and opportunities across four pillars: governance, strategy, risk management, and metrics and targets. The structure closely mirrors the IFRS Foundation’s climate reporting standard for companies, IFRS S2, but is adapted to public sector realities.

The disclosures focus on how climate risks affect an entity’s own operations and financial position, including current and anticipated financial impacts, climate resilience and scenario analysis. Requirements also include reporting greenhouse gas emissions across Scopes 1, 2 and 3, based on the Greenhouse Gas Protocol or an equivalent methodology, subject to transition reliefs.

Read also: EU adopts first-ever standards to certify permanent carbon removal projects

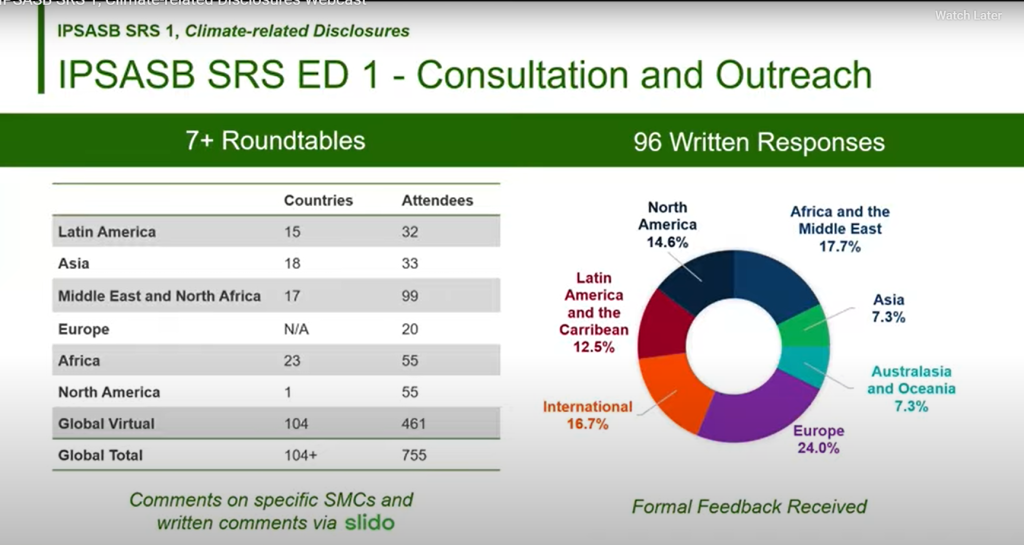

The standard follows a broad global consultation that included regional and virtual roundtables and written submissions from more than 100 countries, with strong participation from Africa. Feedback informed a phased approach that recognises governments’ dual role as operators of public assets and designers of climate policy, with SRS 1 focused initially on climate risks arising from governments’ own operations.

The standard is aligned with the IFRS Foundation’s climate standard, IFRS S2, adopting the same four-pillar structure while adapting it to public sector mandates rather than investor-only reporting.

IPSASB opted to exclude, at this stage, detailed disclosure requirements on governments’ climate-related public policy programmes, such as subsidies or regulatory interventions. Those elements are expected to be addressed in a future phase of the standard following feedback that a phased approach would be more workable for governments with limited reporting capacity.

For African administrations, capacity constraints remain a central concern. Many treasuries and audit institutions are still building basic climate data systems, while line ministries often lack consistent emissions inventories or climate risk assessments. Recognising this, the standard allows governments to delay disclosure of Scope 3 emissions for up to three years and provides flexibility on the timing of first-time reporting.

Despite these transition measures, the direction of travel is clear. Climate risk is being framed explicitly as a public financial management issue, not just an environmental one.

Recent climate events illustrate the stakes. In East Africa, prolonged droughts have reduced agricultural output and increased fiscal pressure through food imports and social support programmes. In Southern Africa, flooding has damaged transport networks, power infrastructure and water systems, raising capital expenditure needs while narrowing fiscal space. Coastal countries, including Senegal and Mozambique, face growing exposure to sea-level rise that could affect ports, tourism assets and urban infrastructure.

By requiring governments to link climate risks to financial statements and long-term fiscal sustainability, the IPSASB standard is expected to push climate considerations deeper into budget planning, debt management and investment decisions.

IPSASB Chair Thomas Müller-Marqués Berger said governments play a decisive role in shaping economy-wide climate outcomes, and that consistent climate-related information is essential for accountability and capital mobilisation. Better disclosures, he said, could support more efficient access to capital markets and help mobilise financing for climate resilience.

The standard is effective for reporting periods beginning on or after January 1, 2028, with early adoption permitted. Several African countries already using International Public Sector Accounting Standards are expected to consider early alignment, particularly those engaged in climate-linked financing, debt-for-climate swaps or sustainability-linked sovereign bonds.

While adoption will be voluntary, development finance institutions and donors are likely to encourage uptake, especially where climate finance is tied to fiscal transparency and governance reforms.

Access the standard, here.

Engage with us on LinkedIn: Africa Sustainability Matters

{kind=link}